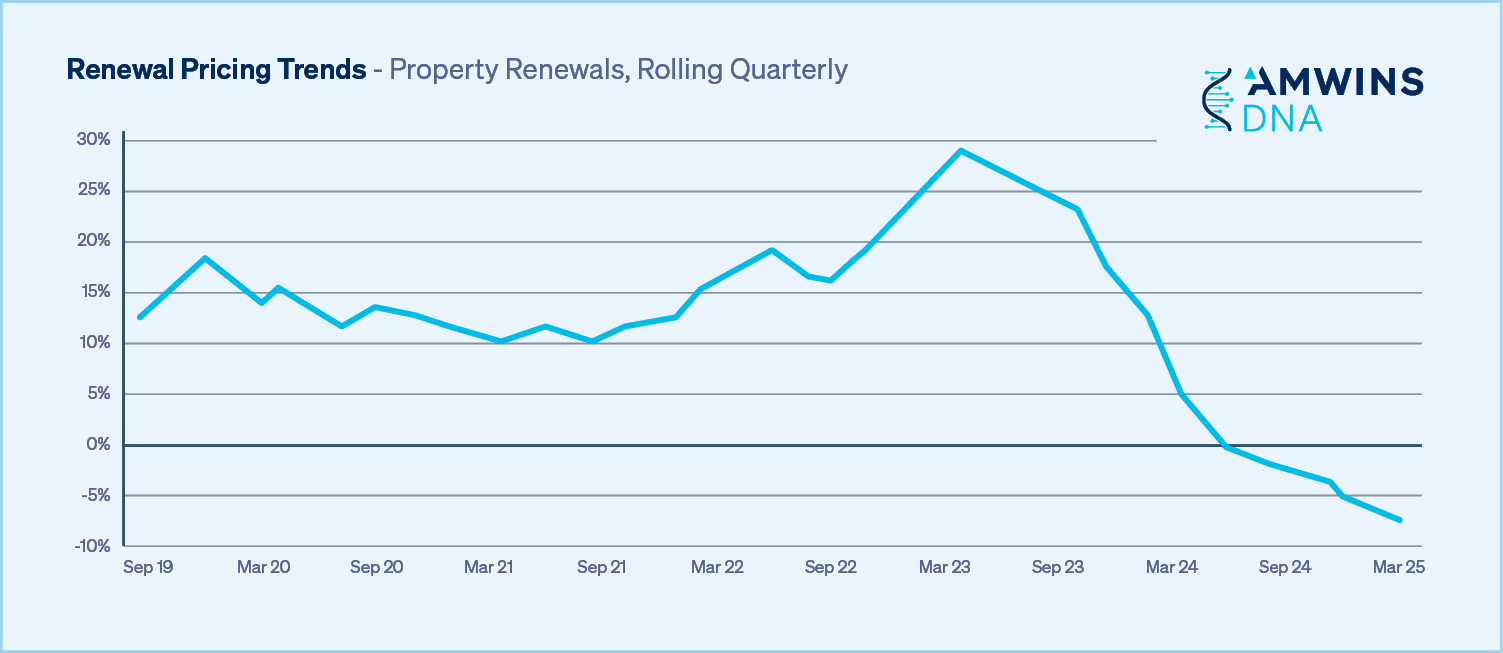

The property marketplace has become extremely competitive, with carriers and MGAs alike heavily focused on account retention and premium growth. Program participants have been forced to quickly become more flexible with pricing, deductibles, terms, conditions and policy form as a result of meaningful amounts of capacity being offered by new carriers and MGA entrants – in addition to line size and appetite expansion from existing carriers and MGAs.

Increased capacity, increased competition

Driven by a wave of new carrier and MGA entrants, combined with many carriers and MGAs rolling out new products, establishing new facilities/programs and expanding carrier appetite/line size , competition within the property space increased meaningfully throughout 2024. That trend has continued into 2025. For example, we have seen select U.S. carriers and Lloyds syndicates re-enter the primary layer multifamily space after sitting on the sidelines for the past several years while other carriers are finding lower attachment points, larger line sizes and/or participation within multiple layers to now be within target.

The soft market showed no signs of stabilizing in March or through the first half of April. Common sentiment is that this is one of the most rapid erosions of property market conditions in decades. A continued downward trend seems inevitable as supply of capacity far outweighs demand and as carriers and MGAs simultaneously attempt to meet the account retention and premium goals established by their management teams. A very telling example is that even loss-affected accounts many times experienced rate decreases in Q1.

Incumbent carriers are fighting hard to retain their renewals and are now more commonly adjusting pricing as necessary to secure renewal orders, with layered and shared accounts often subscribed by 150% to more than 200% in some or all layers. Pressure on terms and conditions is simultaneously increasing, including a heavy focus on deductibles, blanket limits, expansion of coverage in general, a return to program concurrency and the removal of restrictive provisions.

Facultative Reinsurance

The current facultative market closely mirrors the dynamics of the wholesale market with sustained pressure on pricing as well as terms and conditions. Reinsurers remain actively engaged to secure participation on placements, offering solutions that provide meaningful benefits and can prove useful when you’re looking to manage challenging carve-outs for high hazard locations and perils.

Leveraging facultative reinsurance provides strategic value when placing property coverage – despite the soft market. We’re seeing markets capitalize on this to enhance line sizes — specifically to address increased CAT or fire limits on placements.

Macroeconomic Challenges

The macroeconomic climate – marked by ongoing geopolitical tensions, weaking US consumer confidence and uncertainty around recently implemented trade tariffs – is an important consideration for our industry.

While the full impact of tariffs is still developing, early indicators suggest they may negatively affect the insurance market, including the E&S property sector. Amwins is currently working with industry and economic experts to produce a white paper exploring these evolving dynamics.

We believe tariffs could have several downstream effects on E&S Property, including:

- Higher construction costs and replacement costs driven by increased prices for building materials

- Greater need for more accurate property valuations

- Potential for larger claims payouts

- Disruption of supply chains

- Elevated Business Interruption exposures

- Increasing cost of supplies and consumer goods as the result of supply chain delays

- Rising raw material costs

- Regulatory and Compliance challenges

- Emerging legal and regulatory hurdles

- Possible disruption of international reinsurance markets

- Volatility in investment income

While we have not seen direct impacts, we believe it’s reasonable to anticipate future negative effects if the current tariff environment persists.

CAT Losses

In 2024, the US experienced 27 confirmed CAT events with losses exceeding $1B each. CAT losses for H1 2025 are expected to continue the trend of billion-dollar claims – a direct result of California wildfires impacting insurers’ loss budgets early in the year and putting unexpected strain on financial performance. However, all signs indicate that these losses are still within most re/insurers comfort zones.

Losses seen during recent CAT events have only mildly been reflected in treaties while capacity has increased, and demand remains stable. However, if one of those factors changes, losses will matter more as there will be nothing to balance or decrease their impact on premiums.

Severe Convective Storm

Insured losses resulting from national catastrophes reached $140B in 2024, with experts pointing to secondary perils like Severe Convective Storms (SCS) as drivers of rising losses long term. In 2024, SCS alone caused $57B in overall losses in the U.S.; $41B of which was insured loss.

As storm severity escalates, working with insureds to promote and implement more effective and sustainable risk mitigation practices can help reduce exposure and vulnerability to SCS. In addition, and for balance sheet protection purposes, keep deductible buydowns in mind.

Ensuring that coverage is in line with the insured’s expectations can also help. In today’s market, cheaper is not always better. Learn more about how SCS continues to challenge the insurance industry here.

Wildfire

In 2024, nearly 9M acres burned as a result of wildfires – well above the 2.7M acres that burned in 2023. So far this year, more than 8,000 wildfires have burned in excess of 165,000 acres, including the Los Angeles fires which consumed more than 55,000 acres and destroyed close to 16,000 structures with an estimated insured property loss of $45B.

In the first week of April alone, 11 large fires were reported in the U.S., including four in North Carolina and three in Florida. And it’s only expected to get worse; extreme fire events are projected to increase by 50% by the century's end.

Despite wildfires increasing in frequency and severity, insurance rates remain competitive, largely due to significant capacity provided by Lloyd’s and domestic E&S markets. E&S markets are active in this space, offering coverage options in states like California and Nevada where limited capacity as well as high deductibles have been the norm for admitted markets.

You can learn more about the rapid evolution of the wildfire insurance marketplace in our recent market outlook.

The need for flood coverage grows

There were 20 federal flood declarations in 2024, with heavy rainfall, flash floods and urban flooding all driving demand for coverage. At the same time, regions not typically impacted by flooding are seeing an increase in exposure. For example, Tropical Storm Helene dropped more than 30 inches of rain in parts of western North Carolina, causing catastrophic flooding in a region where it’s estimated approximately 2% had flood insurance.

Here’s a short checklist to help ensure that your clients’ property policies provide the flood coverage they need.

- Is flood coverage included within your client’s property program?

- If not, why? Has the insured fully considered this coverage and their exposure?

- If it is, what is the sublimit within their policy? Does a larger sublimit make sense for the insured given their exposure to potential flood events?

- How is surge defined in the policy? Is it included in the definition for wind or flood? If surge is included in the definition of flood, is the flood sublimit amount sufficient to cover an insured’s potential surge loss?

- You can learn more about assessing flood risk and choosing the right option here.

Prepping for the 2025 hurricane season

With the softening market, more Named Windstorm (NWS) capacity has become available and at more competitive rates than we’ve seen in the past two years. It’s important to review these limits with your clients to help ensure that they are appropriately protected based on their current risk profile and budget – especially as we head into what Colorado State University is predicting to be another above-normal hurricane season.

The 2025 CSU forecast calls for 17 named storms, nine hurricanes and four major hurricanes, noting that sea surface temperatures remain warmer than normal, but not as warm as they were in 2024 at this time. When combined with potential La Nina conditions, the environment will be more conducive for hurricanes to form and intensify.

Last year’s hurricane season saw 18 named storms form in the Atlantic Basin, with 11 hurricanes and five major hurricanes. Hurricane Beryl was the earliest storm on record to reach Category 5 strength and back-to-back hurricanes Helene and Milton caused unprecedented property damage. However, despite the active season, 2024 was seen largely as an earnings event, rather than a balance sheet event, for most carriers.

As we face the start of the 2025 season, the National Hurricane Center has announced a few updates that should enable clients to better prepare for potential impact:

- Advisories will be issued up to 72 hours (not 48) in advance of a system with tropical storm force winds or storm surge that is likely to make landfall.

- Cones of uncertainty will be 2% to 6% smaller, allowing for greater accuracy in naming potentially affected areas.

- Updates to rip current maps and improved computer modeling will also allow for more precise forecasting.

London

Similar to 2024, London remains a competitive market and has quickly adapted to softening conditions. While most syndicates and companies claim they were not anticipating this unprecedented pace of softening, the general view is that a margin of profitability still remains in the current rating environment.

On average, London is experiencing significant rate reduction on renewals. Leveraging new syndicate/company pricing to reduce incumbent pricing is regularly in play to achieve required rate reductions. At the same time, last-minute reductions in quoted pricing to secure firm orders are also becoming more widespread.

Accounts with very substantial losses in 2024 are seeing some rate increases, nevertheless most loss-affected accounts are remaining flat or even seeing rate reductions. Valuation conversations have remained minimal for most markets; however, as lumber pricing returns to the spotlight following recent tariffs, this could change in the near future.

Other items of note include:

- Terms and conditions: Coverages, sublimits and deductibles have all relaxed since this time last year as carriers are more open to negotiations.

- Wildfire: London D&F markets were not impacted by many of the wildfire losses earlier in the year and there hasn't been a noticeable drop in willingness to underwrite this peril.

- Single peril covers: We have seen more willingness to write single peril covers (e.g., NWS only) than in prior years.

Finally, London experienced a further increase in follow form automatic capacity in Q1. For example, Amplify, Amwins’ in-house facility, can now offer up to $10M USD capacity on any one risk. Other examples include Ki (algorithmic syndicate), which has increased its capacity behind a growing panel of lead markets and Insurex which provides automatic follow facility behind Inigo and Atrium syndicates.

Very few classes of business are off limits, and there is no sign that the new business flow is slowing down. London remains a market eager to retain and even grow its footprint in the E&S marketplace.

Bermuda

Since the beginning of the year, several Bermuda markets have budgeted rate reductions. These same markets are now being pressured to reduce rates even further. Market appetite remains generally the same, with a focus on either CAT heavy buffer layers with $5M to $15M line sizes or attaching in excess of probable maximum loss (PML) with large line sizes from $25M to $600M.

Heavy CAT accounts that received significant discounts over the past one to two years are experiencing further rate reductions. When dealing with long-term incumbents, Bermuda markets may also reduce line sizes in order to maintain relationships with core accounts.

Bermuda markets have been especially successful with DIC accounts (SCS, NWS and earthquake only accounts), capacity driven accounts and distressed classes. Markets are also trying to recuperate lost revenue with lower attachment points or increased line sizes at renewal and there has been significant pressure to remove the Values Limitations Clause, which most have agreed to do.

Tap into Amwins’ expertise

Placing nearly 100,000 property accounts via more than 425 markets each year, Amwins studies property market conditions and industry trends to identify solutions for your clients' most challenging risks. When you tap into our network of property specialists, you gain access to unmatched size, market access, resources and leverage, all deployed to best address your clients’ unique needs.

Our property insurance expertise extends to catastrophe-driven accounts with an in-house actuarial team that not only runs modeling analyses for wind exposures through RMS and AIR but also interprets the results and prepares a detailed report for your review. We also push the boundaries of traditional insurance with our parametric solutions that can help round out risk transfer to better cover the inevitable unknowns and the unexpected.

Amwins Re, a national reinsurance broker, specializes in the placement of facultative property reinsurance and program administration. They leverage creativity in problem solving, including carving out perils and locations, blending coverage to reduce gross premium, lowering deductible through a buydown and much more. Their top areas of specialty include, but are not limited to:

- Small accounts to layered and shared accounts

- CAT-exposed schedules

- Builder’s risk

- Real estate/habitational

- Public entity

- Manufacturing (including food processing and lumber/sawmills)

Amwins also offers exclusive capacity and property programs through Amwins Special Risk Underwriters (SRU). Their capabilities include all-risk property and wind-catastrophe perils (ground-up, primary, buffer, excess, quota share, earthquake and deductible buydowns. You can learn more here.

We also recently announced CoverCap, an exclusive E&S solution providing ground-up or primary layer property coverage for smaller commercial risks with total insured values (TIV) below $50 million. Designed to deliver up to 100% support of a $50M limit, this program is available exclusively through Amwins brokers and backed by an AM Best “A” rated carrier partner.

We help you win

As the nation’s leading wholesale broker, relationships are our strength. To meet your clients' evolving needs, Amwins puts our market relationships and clout to work by continuously developing proprietary products and delivering exclusive capacity.

We give you a distinct advantage over your competitors. Contact one of our property specialists today.

Be on the lookout

- Large TIV multifamily and real estate accounts that are currently placed in the Admitted marketplace may now be better suited for the E&S marketplace as E&S carriers have become increasingly competitive.

- The size of primary layers are often being stretched, for instance from $5M to $10M or $10M to $25M, as well as from $25M to $50M.

- The number of new carriers, MGAs and products (i.e., appetite expansion) that have entered the property marketplace over the past 24 months is unprecedented. That said, keep in mind that most of these new sources of capacity are limited distribution in nature. Amwins continuously receives these appointments, ensuring our ability to deliver the very most competitive solutions for you and your clients.

- With submission flow at or near an all-time high, quality submissions continue to be a key differentiator. Underwriters gravitate to detailed and nicely organized submissions.

- Frequent communication and expectation setting with your insureds is critical, including detailing the strategies, approaches, anticipated results and full market access that will be aggressively tested during an extensive marketing effort.

- During soft market conditions, it’s important not to lose sight of loyalty to long-term incumbents and carriers that have paid meaningful claims.

- While tempting to reduce the number of carriers utilized in layered and shared placements during soft market conditions, it’s worth considering how to continue spreading orders across many markets to help ensure that there is not too much reliance on any given carrier or marketplace. Keep in mind for instance that every soft market is eventually followed by a hard market.