Recent reports are challenging the traditional classification of perils and calling into question how the insurance industry defines catastrophic risk. Why? Because secondary perils – specifically severe convective storms (SCS) – are becoming much more frequent and even more severe.

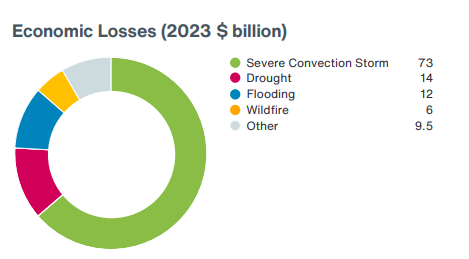

In 2023, these storms – characterized by strong winds, tornadoes, hail and heavy rain – dominated global insured losses, surpassing $50B in losses within the U.S. alone and making up nearly 60% of all insured losses. The trend has continued in 2024, with 13 individual billion-dollar loss insured SCS events exceeding $30B in insured losses in the first half of the year.

Frequency and severity continue to raise concern

The cost to address damage done by SCS is now almost on par with primary perils like hurricanes and earthquakes. It has been suggested the terms “peak” and “non-peak” perils rather than “primary” and “secondary” perils may be more accurate.

There has also been an increase in losses caused by sub-perils like hail. With a peak season of March through June, the SCS sub-peril hail produces the largest loss and typically accounts for 50% to 80% of SCS claims. In 2023, the U.S. recorded more than 1,000 large hail reports with the Southern Plains and Southeast being the hardest hit.

Market effects

The property market has stabilized through 2024. We haven’t seen wholesale rate changes as a result of the growing losses attributed to SCS; however, deductibles are increasing – especially in markets like Florida and Texas – and full limits can be hard to come by.

Global reinsurers have experienced robust overall performance in the past 18 months, despite heightened activity and increased losses. Structural changes, including higher attachment points, lower limits, tighter terms, fewer aggregate covers and risk repricing, are all contributing to these performance improvements.

Similarly, a lack of consistent SCS modeling, limited historical data and ongoing changes to definitions of high-risk areas, have left treaty markets cautious when it comes to SCS and primary coverages often bearing the brunt of any loss. Add to that the fact that some carriers are exiting the most risk prone markets at the same time others are reducing line size to help ease volatility, and it now takes multiple carriers to provide full cover.

Risk mitigation strategies can help

E&S markets are typically more flexible, innovative and responsive to the changing needs and demands of insureds. This is especially true for complex risks like SCS facing challenges such as:

- Substantial losses and claims from insureds across different regions and sectors

- Reduced capacity and increased exclusions

- Updates to traditional risk assessment and modeling

Working with insureds to promote and implement more effective and sustainable risk mitigation practices can help reduce exposure and vulnerability to SCS. For example, replacing composition roofs with a heavier class roof not only helps prevent damage, but it can also make an account more attractive to underwriters. Similarly, implementing modern building codes and enforcement is crucial.

Ensuring that coverage is in line with the insured’s expectations can also help. In a changing market, lower premiums may not always provide the necessary cover. Insureds should understand:

- ACV (actual cash value) and cosmetic endorsements can limit coverage

- Up to date valuations are a must as construction costs continue to rise

- Risk prone areas will have higher deductibles than regions with lower loss ratio

- Per location deductibles are more prevalent than per occasion deductible in high-risk areas

- Deductible buy-backs may help to level wind exposure costs (e.g., lowering a 5% per location deductible to 2% or 3% deductible).

Insureds may also want to consider:

- Self-insuring certain properties or covering the cost of repairs without filing a claim. For example, a small shed on a property may not require commercial coverage as the cost to replace it would be less than the windstorm deductible or even the premium.

- Taking advantage of data and analytics to help improve risk identification, evaluation and pricing.

- Purchasing parametric insurance to complement traditional insurance and help offset uninsured expenses.

Partner with a wholesale broker

Working with a partner like Amwins gives you an advantage. With the largest specialty insurance distribution platform in the industry, we stay on top of market conditions and trends to keep our retailers ahead of the game.

Amwins’ value-added resources, market relationships and solutions get tough deals done. Our in-house team of actuaries licenses cutting-edge software to deliver catastrophe risk data analysis and the most accurate pricing possible. And by analyzing data from thousands of Amwins-placed accounts, we bring our clients valuable insight through tools such as benchmarking reports and price trends.

We work with you, so you win.