Flood insurance is an essential safeguard for property owners, yet many misunderstand the differences between primary-only coverage and a combination of primary and excess coverage. With varying limits, coverage scopes and policy structures, choosing the right option can significantly impact financial protection in the event of a flood. Understanding these distinctions is crucial to ensuring adequate coverage, whether through the National Flood Insurance Program (NFIP) or private market solutions.

This article was produced in partnership with Amwins InstantQuote, a fast and efficient platform for securing flood insurance solutions.

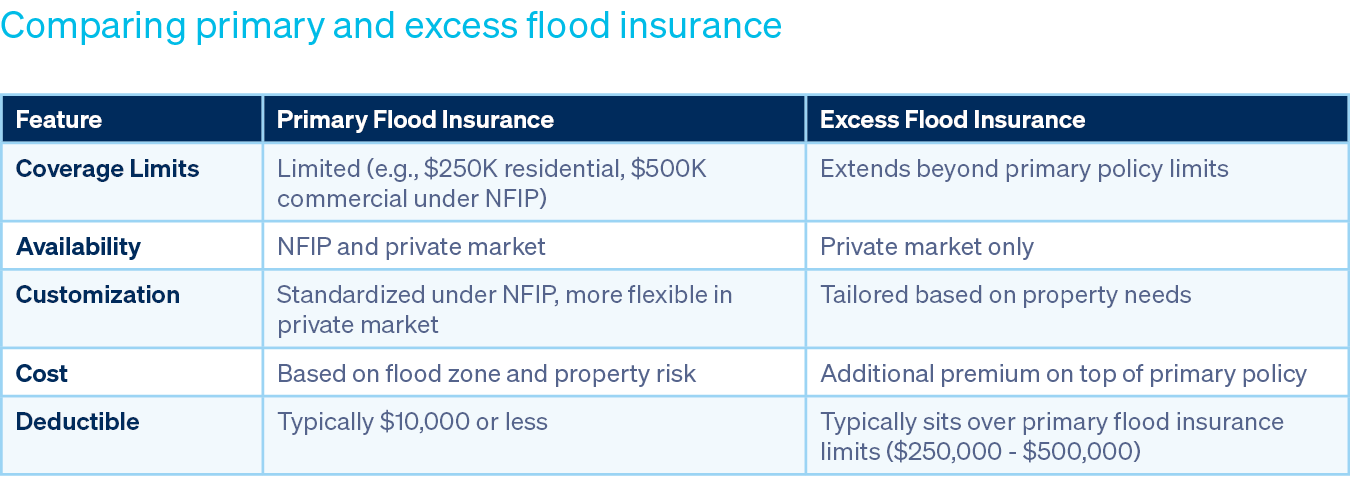

Primary flood insurance

Primary flood insurance is the foundational layer of coverage that provides the first level of financial protection against flood damage. This coverage is always required by mortgage lenders for properties in high-risk flood zones. NFIP coverage, administered by FEMA, offers standardized flood policies with set coverage limits, providing up to $250,000 for residential structures and $500,000 for commercial buildings, with additional limits for personal and business property. These policies are subject to waiting periods, exclusions and strict underwriting criteria.

Private market insurers offer primary flood policies that may provide higher limits and additional coverage options. These policies can include broader protection, such as loss of use, business interruption or higher personal property limits. They may also have different underwriting guidelines, pricing structures and availability based on location. One key distinction of primary flood policies is the deductible, which is typically $10,000 or less, making it more accessible for policyholders to file claims without excessive out-of-pocket costs. By providing access to competitive private flood solutions, Amwins IQ helps policyholders find tailored solutions beyond NFIP limitations.

Primary + excess flood insurance

Primary flood insurance with the addition of excess flood insurance policies provides additional coverage beyond the limits of a primary-only policy. It is designed for policyholders who need more protection than what is available through NFIP or a private primary policy. Excess flood insurance is available for residential and commercial properties that exceed NFIP or private primary limits. It covers the portion of losses not reimbursed by a primary policy, ensuring greater financial protection. Excess coverage can only be purchased from private insurers, underwriting is based on property value, location and flood risk. Once the primary policy is maxed out, the excess policy kicks in, where the primary coverage acts as a deductible. This additional layer of coverage is particularly valuable for high-value properties or businesses with substantial flood exposure, offering peace of mind that financial recovery will not be limited by standard policy caps. Unlike primary policies, excess flood coverage typically require the underlying limits to be exhausted ($250,000 for residential, $500,000 for commercial), limiting out-of-pocket cost to the underlying policy’s deductible.

Gaps in homeowners’ insurance for flood losses

Many homeowners mistakenly believe their standard homeowner’s insurance policy covers flood-related losses. However, all traditional homeowners’ policies explicitly exclude flood damage, leaving property owners vulnerable in the event of a disaster. Without a separate flood insurance policy, homeowners may face significant out-of-pocket expenses to repair structural damage, replace belongings and recover from financial setbacks. This gap in coverage underscores the importance of securing primary flood insurance, particularly for those in moderate-to-high-risk flood zones.

Understanding your flood risk

Many property owners do not fully understand their flood risk until they experience a loss firsthand. Flood risk is not limited to coastal areas or high-risk flood zones. Severe weather events, changing climate patterns and urban development can all contribute to unexpected flooding in areas previously considered low-risk. Reviewing FEMA flood maps, consulting with insurance professionals and considering private market flood insurance options can help property owners make informed decisions and ensure adequate protection against flood-related financial losses.

Selecting between primary and excess flood insurance depends on property value, location and risk exposure. Policyholders in high-risk areas or those with significant assets may benefit from excess coverage to ensure full protection. Amwins IQ simplifies the process by offering instant access to both primary and excess flood insurance options. We have experts to help retailers gauge what the flood risk really is for their policyholders, ensuring the right coverage for every situation.

Takeaway

Flood insurance is not a one-size-fits-all solution. While primary coverage provides essential protection, excess flood insurance plays a crucial role in mitigating financial risks for properties with higher values. Understanding these distinctions helps property owners and businesses make informed decisions about their flood coverage needs.

The Amwins advantage

In today’s competitive insurance market, speed and accuracy matter. With Amwins IQ, you get instant access to top-tier coverage options, including private primary flood insurance for residential risks with NFIP-equivalent and higher limits. Our flood solution offers instant binding up to $2 million, giving you the flexibility and speed needed to serve your clients effectively. Let us do the heavy lifting so you can focus on winning more business. Get started today at Amwins.com/quote-online.