While some segments are seeing softening, others face the hardest market conditions in decades. In this State of the Market report, Amwins specialists share market intelligence spanning rate, capacity, and coverage trends across lines of business and industries.

As we anticipate 2025, capturing the nuances of an ever-changing market remains a challenge. Some industries are seeing a competitive rate environment and better underwriting conditions, while others are contending with the exact opposite.

This comprehensive State of the Market report presents expert analyses from Amwins specialists on the factors shaping these market conditions. They provide critical insights into rate trends, capacity and shifting coverage patterns across multiple lines of business, industries and risk specialty practices in the United States, London and Bermuda.

Our goal is not merely to predict market trends but to uphold our commitment to you. With five core divisions, 100+ underwriting programs and a worldwide reach, our dedicated practice groups, brokers and underwriters have the expertise, knowledge and relationships of the firm at their fingertips — giving you a distinct advantage.

We are committed to delivering the best products and services available, regardless of prevailing trends and market conditions, and to help you navigate the challenges and changes that lie ahead.

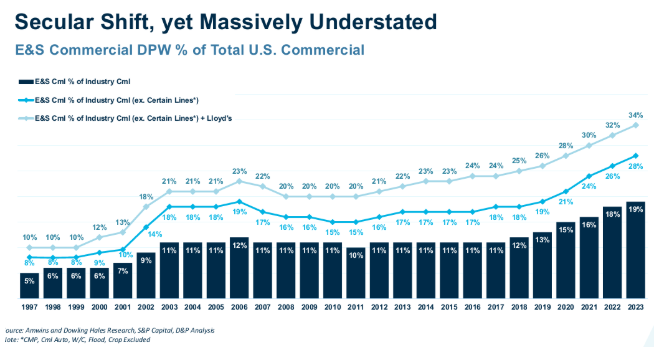

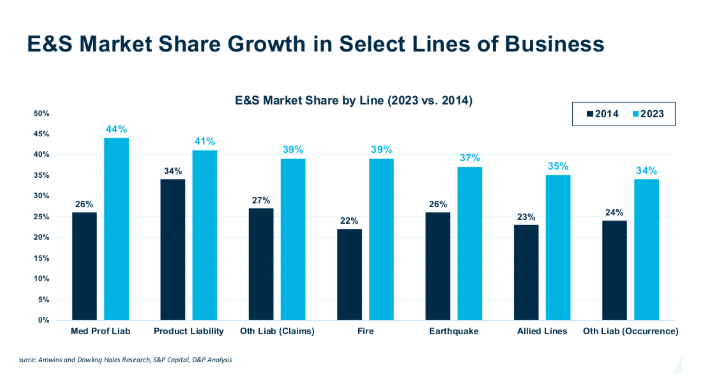

Shift to E&S markets continues

The Excess & Surplus (E&S) insurance market has experienced notable growth over the past six years, driven by a confluence of factors that have reshaped the risk landscape and expanded demand for specialized coverage. Earlier this year, Dowling & Partners reported that an estimated 34% of U.S. commercial business is E&S while AM Best reported the U.S. surplus lines market produced more than $115B in premium in 2023.

One of the key drivers of this growth is the commitment carriers have to the model. In 2003, there were only four carriers with wholesale strategies. That number grew to 13 in 2022, with more than $35B in direct premiums written (an increase of more than 11.5x).

This is especially true as small and mid-size business risks have grown in complexity and size, as has the level of risk in certain lines of business. Increased casualty risk has been primarily driven by social inflation and technology advancements while growing property risk can be attributed to the increasing severity of natural disasters like hurricanes and wildfires. The E&S market, with its flexibility and capacity for innovation, has stepped in to address these gaps effectively.

Another driving factor is the market’s expertise in underwriting complex and non-standard risks. E&S insurers have the ability to craft customized policies and respond quickly to market changes – making them appealing to the growing number of clients seeking coverage for unique exposures.

At Amwins, we’ve harnessed the power of data through

Amwins DNA to build capacity and create new and exclusive products and programs – ensuring that we find the best solutions for our clients and their insureds.

Be on the lookout

The future of the E&S insurance market is positive, with several factors likely to sustain its growth trajectory:

- innovation in product development to address emerging risks

- Expansion into new and underserved markets

- Leveraging technology and data analytics to enhance underwriting accuracy and efficiency

- Ongoing adaptation to changing regulatory landscapes

With a strong foundation and a forward-looking approach, the market is well-positioned to continue its upward trajectory.

Property

The property market continues to be fragile; however, it is softening overall. We will be presenting a more in-depth analysis of the property market in Q1 2025.

Financial impacts of back-to-back hurricanes

Hurricanes Helene and Milton couldn’t have been more different. While both were significant weather events that caused a lot of property damage, Helene was primarily an inland flood event with initial loss estimates of $6B to $12B and Milton was more of a wind event with loss estimates ranging from $15B to $30B.

After making landfall as a Category 4 hurricane in Florida, Helene worked its way north, dropping more than 30 inches of rain in areas of western North Carolina. Not traditionally considered a hurricane impact or flood zone, the Insurance Information Institute has estimated that only 1% of homeowners in NC who sustained flooding from Helene were insured. As a result, state and local governments are expected to bear the brunt of the losses and have begun to apply for and receive federal funding from FEMA for cleanup and restoration efforts.

Milton made landfall as a Category 3 hurricane near Siesta Key, FL, after making a southward turn that avoided what could have easily become one of the worst CAT events in U.S. history. Initially slated to make landfall in the Tampa area, much of the damage that did occur was focused on less populated areas on the west coast of the state and will likely be attributed to the homeowners’ market. We expect that – at the very least – Milton will serve as

a reinsurance event for Florida domestics but overall will not affect the balance sheets of most reinsurers.

Overall trends still ring true

Despite pending losses from Hurricanes Helene and Milton – as well as other named and severe convective storms (SCS) this season – the property market has continued to soften overall. New capacity continued to enter the space in 2024, forcing existing markets to become more flexible with their pricing and overall appetites. Many carriers also increased their line sizes, making layered and shared deals easier to place.

Rates remain softer on the East Coast than the West as well as for insureds with large TIV overall. Small TIV accounts, however, continue to face challenges, and we expect that market will continue to harden.

While the possibility exists that the combination of Helene and Milton may affect the property market to some extent in ‘25, it is still too early to be certain of the exact impact. For now, we view the ’24 hurricane season as an earnings event, rather than a balance sheet event, for the vast majority of carriers.

Regardless, as claims move through the system and projections of financial impacts become a reality, Milton will be considered one of the top 10 costliest hurricanes in U.S. history; however, the lack of absorption from the reinsurance marketplace means that it hasn’t dented carrier profits and there is no fear of continued softening.

London

London remains an important market in this class (across both primary and excess layers) and there is no sign that market appetite for writing new opportunities is likely to diminish in 2025. So far, 2024 has been a profitable year for the vast majority of carriers and although the pricing peak has come and gone, the view of many underwriters is that there are still adequate margins to retain this profitability.

There is no doubt that the rating environment has become much more favorable for clients after many years of hardening terms, particularly for those insureds unaffected by Hurricanes Helene and Milton and, although it is still too early to evaluate how the reinsurance market will react at the end of year renewals, the expectation is that any savings made at the January 1, 2025 renewals will be passed on by the primary carriers.

While there are only a handful of new entrants in the London market, the MGA and follow form environment is vibrant and the majority of Lloyd’s syndicates and London company markets have expressed a willingness to grow in 2025 – particularly if terms and conditions remains relatively favorable. It is expected that any improvement in terms for insureds will first and foremost come in the form of premium savings; however, all elements of the program (including sublimits and coverages) will likely form part of the broker/underwriter negotiation going forward.

The conversations around valuations have not disappeared but general consensus within London is that much of the remedial work has been done and as long as acceptable price per square foot is being proposed from the outset, the focus will return to the normal underwriting criteria of occupancy, risk management, loss history, pricing and capacity deployment. The implementation of RMS 23 has been slower than anticipated; however, general belief is that this is producing higher technical pricing outputs and could potentially be set at odds with the softening rating environment.

Bermuda

Current conditions are putting pressure on the Bermuda market. In 2024, Bermuda carriers have been quoting on average flat to 5%-10% rate decrease, with many accounts seeing flat premium renewals where TIV has increased. Distressed accounts, on the other hand, have seen rate increases to ensure rate adequacy.

Bermuda is having success with CAT driven placements that are being restructured or have significantly grown year over year. Underwriters have not seen a significant impact on their books as a result of hurricanes Helene and Milton.

Be on the lookout

Since Hurricane Ian in 2022, many reinsurers have imposed higher attachment points on carriers for catastrophic coverage. This has caused a shift in how these storms have affected the insurance market compared to the past. Experts now believe it will take a series of combined events – both large and small – to result in a slight hardening of the market or a slowdown in the softening of the market overall.

Insurance markets are continuing to absorb the majority of losses caused by hefty SCS losses and it would likely take a catastrophic event – or a series of small events – with damages in excess of $100B to move the market substantially.

Insight provided by:

- Kayla Bridgewater, VP, Amwins Bermuda

- Toby Colls, Managing Director, Worldwide Property, Amwins Global Risks

- Alan Mooney, CEO, Amwins Bermuda

- Harry Tucker, EVP and Amwins National Property Practice Leader

- Jessica Zuiker, VP and Assistant National Property Practice Leader

Casualty

Market conditions

The casualty insurance market remains in a state of adjustment as we move into 2025. Loss development continues to be driven by a host of challenges ranging from social inflation to the overall complexities of the legal environment. It’s clear that current rate increases are here to stay for the foreseeable future.

There is optimism among carriers about the rate environment, driving a sustained push for rate across their portfolios. However, some uncertainty looms over reinsurance treaty renewals, with cautious sentiment stemming from loss development issues from 2019 to 2022. While capacity remains available, carriers are selective, especially with auto-exposed risks. The focus on middle-market business, with premiums ranging from $25,000 to $100,000, continues to grow and will likely maintain a competitive edge through 2025.

Challenges

Traditional carriers continue to face competition from recent market entrants, leading them to emphasize their financial strength, claims handling and long-standing presence in the E&S space. This competition is driving concerns about adverse selection and the ability to maintain a diverse and profitable casualty portfolio. Primary general liability is a particular pain point, with key markets implementing higher retentions, stricter terms and pricing increases for frequency-driven classes due to rising claims costs. Submission management also remains a significant challenge, as submission activity continues to grow in the double digits. Most carriers now rely on broker relationships to help identify opportunities and are experimenting with AI-driven prioritization to manage the flow of submissions within their target appetite.

Be on the lookout

Excess layers have retained strong rate relativity, with the percentage cost of an excess layer continuing to hold firm relative to the layer beneath it. As capacity continues to be monitored in the excess spaces, we are seeing a regained focus on tightening appetite in the primary layer.

A tough legal environment

Social inflation continues to be a significant concern for carriers and reinsurers, particularly in states with plaintiff friendly legal venues, such as

Georgia, Pennsylvania and California. At the heart of this issue is not only nuclear verdicts but third-party litigation funding, which has introduced new complexities to the legal landscape. The issue isn’t simply the existence of litigation funding itself, but the disclosure (or lack thereof) in individual court cases, which can skew the playing field and contribute to the rising cost of claims.

Indiana, Louisiana and West Virginia enacted reforms at the state level this year to address litigation funding, and legislation was recently introduced at the

federal level for more transparency in federal cases. While these are encouraging developments, more states will need to address the issues of litigation financing and tort reform before we see any meaningful impact to the casualty market.

Capacity

Unlike the property market where there is a growing sense of confidence among carriers and rate stabilization for many sectors, carriers within the casualty market cannot yet claim with certainty that their book is stable and prepared for the future.

Over the past few years, many carriers have reduced line sizes and shifted their mix of exposure from long-tail to shorter-tail risks. While these measures have provided some relief, they have not fully addressed the underlying issues, leaving few carriers willing to say they feel fully confident in their casualty portfolios.

That being said, there are some players within the market that are becoming more aggressive, hoping to capitalize on current rate conditions. However, the overall market is not yet stable enough to inspire broad optimism. On the positive side, solutions are being found and capacity is available, though it often comes at a higher cost than clients desire.

While the market is far from perfect, it isn’t entirely pessimistic. The ongoing inflow of investment and new entrants signals that there is still enough appeal in the market to sustain optimism for the future, even if caution is warranted.

Be on the lookout

New capacity is still entering the market, both on the direct carrier and MGA sides, and we're seeing more innovative approaches to finding solutions. Programs aggregating homogeneous, profitable business or creative risk structures where insureds take on more financial participation are helping to provide coverage where it's most needed.

Carriers are beginning to explore new pockets of opportunity in the middle market, particularly in classes like commercial construction. With reduced uncertainty in these sectors, more competition is emerging, and markets are finding ways to shift their focus to these relatively stable segments in an attempt to balance their books against more distressed areas.

London

London is poised to become a more visible player in the casualty market over the next year, especially in challenging sectors like transportation and real estate. With new syndicates and capacity entering the space, London-based insurers are expected to help fill gaps in towers, particularly for harder-to-place risks.

With this increased presence, London will be able to offer solutions where capacity has been tighter – making it an attractive option for excess placements and difficult-to-place risks such as standalone sexual abuse and molestation (SAM) coverage.

Bermuda

While most insureds are still seeing rate increases, the pace of these increases has slowed, and average rate increases are now in the 5% to 7% range. For tough classes or accounts with adverse loss experience higher rate increases can be expected.

The market in Bermuda continues to evolve with the addition of two new entrants in the last 12 months, both operating under the MGA model. This has increased the number of traditional casualty insurance markets in Bermuda to 20. These new entrants have primarily served to fill gaps in towers as a result of capacity reductions from incumbent markets in recent years.

As with domestic markets, Bermuda carriers are continually seeking to balance their books to manage the effects of social inflation and nuclear verdicts. Carriers are also continuing to see the impact of litigation funding and are adjusting their capacity offerings as a result.

Average capacity offered now ranges from $5M to $10M. In some cases, Bermuda markets will offer up to $25M or more depending on the class and position in the tower. Exposure to multiple claims from the same event that affect more than one client is an ongoing issue for carriers and will impact the amount of capacity on a given account.

Bermuda continues to be a go-to market for creative, alternative risk transfer solutions as an increasing number of insureds seek out alternative risk management solutions as guaranteed cost premiums continue to rise. The use of retention vehicles, such as captives, in a casualty tower has also become more common for middle market clients seeking a longer-term solution to manage increasing deductibles and self-insured retentions.

Be on the lookout

Retailers should brace for a more aggressive push in primary rate increases over the next 12 months. While excess rates have remained in the mid-teens for several years, primary rate adjustments have lagged (in the low-to-mid single digits). This disparity is unsustainable, especially as primary rates drive the structure of the tower.

We expect to see primary rate increases hit double digits in 2025 as capacity continues to focus more on excess rather than primary coverages. Rate relativity remains strong, with the percentage cost of excess layers maintaining their relationship to the layers beneath them.

The longer tail nature of casualty claims means that loss latency will continue to be an issue. Property losses are typically easier to quantify and predict, while casualty remains more unpredictable, often with delayed impacts. The tail on casualty business continues to grow and carriers are increasingly on the lookout, especially as primary rates push higher than they have in recent years.

Insight provided by:

- Tom Dillon – EVP and Amwins National Casualty Practice Leader

- Helen Fry – SVP, Amwins Special Risk Underwriters

- Alan Mooney – CEO, Amwins Bermuda

- Nate Schepers – VP and Amwins Assistant National Casualty Practice Leader

Professional Lines

The professional lines market is entering a period of transformation as carriers adapt to new opportunities and challenges. As growth and innovation stay top of mind, we’re seeing notable trends emerge.

Carriers are beginning to prioritize the diversification of risk portfolios. Many are exploring smaller risk where they traditionally worked with larger ones, and carriers who commonly dealt with smaller risks are moving upstream. Additionally, markets are starting to explore previously untapped sectors, such as healthcare D&O.

Enhanced offerings with additional digital security services and preventative options are also emerging, aimed to differentiate the carrier beyond mere policy language. Some markets are even tapping into independent revenue streams from these services, reflecting a broader trend towards diversification.

The importance of data and transactional efficiency is also becoming increasingly recognized. Markets are investing in advanced technologies, such as artificial intelligence (AI) and application programming interfaces (APIs), to streamline online portals and improve user experiences. This technological focus not only enhances efficiency but also positions carriers to better compete with emerging insurtechs.

Strategy and specialization

In the realm of distribution, a clear distinction is being made between wholesale and retail strategies. While some markets remain open to retail business, there is a clear focus on differentiating wholesale appetite and transactional speed. This strategic approach allows carriers to better cater to the needs of their wholesale channels.

As the market shifts, specialization is becoming key. Carriers are keen on carving out niches in areas like telemedicine and real estate development. The current soft market climate drives innovation, with an emphasis on managing limits for tougher risks.

Be on the lookout

In this competitive environment, markets are striving to win deals while being mindful of the lessons learned from past market cycles. There is a push to remain competitive; however, many carriers are reluctant to chase excessive price decreases that could jeopardize long-term stability.

Recognizing the importance of strong partnerships, markets are hiring more underwriters and prioritizing service and relationship building. This focus on collaboration ensures that carriers can respond effectively to time-sensitive situations, fostering trust and reliability with their brokers.

Insights provided by:

- Selvin Green, AVP and Amwins Assistant National Professional Lines Practice Leader

- David Lewison, EVP and Amwins National Professional Lines Practice Leader

The Directors and Officers (D&O) marketplace remains competitive as a result of excess capacity and new market entrants. This influx of new players prioritizing private D&O coverage is raising the levels of competition across the board – management liability is currently being offered by more than 85 markets and signs point to ongoing growth.

Capacity and pricing

New capacity is flooding an already saturated marketplace, creating significant downward pressure on rates. As a direct consequence of this intense competition, insurers are increasingly offering price reductions to fend off marketing efforts from rival carriers. Many incumbents find themselves in a position where they must offer competitive pricing and favorable terms just to retain business.

The dynamic pricing landscape also reflects a broader shift in how insurers assess risk. Established carriers are reevaluating their pricing strategies to respond to the new competitive reality, leading to overall rate decreases across an assortment of targeted profitable segments.

Coverage limitations

The continuous entry of new players — particularly MGAs and insurtechs — has reshaped traditional underwriting practices and contributed to the softening of the market. These new entrants are leveraging technology and data analytics to enhance their underwriting capabilities, further intensifying competition. As advancements continue to be made and technologies mature, these tools are likely to play a more critical role in risk assessment and claims management.

At the same time, most underwriters are actively expanding their coverage options to attract business. Insurers recognize the need to differentiate themselves in a crowded market, leading to enhancements such as lower self-insured retentions (SIRs) and higher sublimits for various coverages. This broader approach allows carriers to appeal to a wider array of potential clients.

However, there are some outliers. We have seen emerging limitations focused on claims related to biometric data. Insurers operating in states like Illinois and California have become more cautious, imposing specific exclusions tied to these risks.

Economic impacts

Social and economic inflation are both significant factors for the D&O sector. Rising claims costs, driven by increasing verdicts and settlements, complicate the underwriting landscape. Additionally, businesses are grappling with rising operational costs associated with inflation, which can lead to greater financial instability and an uptick in claims.

The current economic climate, powered by inflationary pressures and higher interest rates, has also led to an increase in bankruptcies. Companies facing maturing credit facilities may find bankruptcy their only viable option, raising the potential for claims under D&O policies.

A key consideration for policyholders is to avoid accepting creditor or bankruptcy exclusions during renewals. Such exclusions can expose individual directors and officers to personal legal liabilities if the company cannot indemnify them. Some markets are open to discussing terms that allow for greater coverage, even for companies emerging from bankruptcy, provided there is a compelling narrative for recovery.

Unique risks and nuanced solutions

Despite increased competition overall, there are still sectors facing challenges. In California, for example, the appetite for private D&O coverage, especially policies that include Employment Practices Liability (EPL), remains somewhat constrained. Insurers are narrowing coverage while simultaneously setting higher retentions which complicates the insured’s ability to secure more favorable terms. Building strong relationships with underwriters is becoming critical for brokers and clients alike.

Public D&O coverage for Special Purpose Acquisition Companies (SPACs) also presents a unique risk as insurers have a limited appetite for this type of risk. A more nuanced underwriting approach is required as regulatory challenges and heightened scrutiny continue to make the landscape more complex.

Addressing these challenges comes down to prioritizing a narrative that points to robust risk management strategies. By effectively communicating their risk profiles and growth plans, stakeholders may negotiate better terms – even in more competitive segments.

London

In London, pricing has continued to soften, with both primary and excess layers seeing reductions due to strong market competition. While the rate of decrease in excess layers has slowed compared to previous years, there’s enough capacity to maintain relatively stable pricing across most accounts. No significant shifts have been reported within policy exclusions; however, claims trends are expected to play a key role in shaping the market's development over the coming years.

Be on the lookout

While we expect the D&O landscape to remain competitive in the near future, there are signs that market stabilization may be on the horizon. Claims development trends indicate a potential shift in the balance of risk and reward, which could lead to a recalibration of underwriting practices.

Insights provided by:

- Seth Brickman, Managing Director, Business Risk Partners

- Jenny Fraser, AVP, Amwins Brokerage

- Scott Misson, EVP, Amwins Special Risk Underwriters

- Joe Robuck, EVP, Amwins Brokerage

- Corey Turner, SVP, Amwins Brokerage

EPL

The Employment Practices Liability (EPL) insurance market is currently experiencing a softening phase, characterized by decreased rates and increased competition. While tougher conditions were previously evident, the influx of new market entrants has intensified pricing pressures, resulting in more competitive rates across various classes and regions. However, this more competitive landscape isn’t without challenges, as inadequate policy coverage may become the norm in the bid for new clients.

We continue to observe dips in pricing as insurers move to increase capacity, thereby capturing more business. Notable changes to coverage limitations have not occurred on a broad scale, but exclusions are becoming more common. A prime example of this is the

Biometric Information Privacy Act (BIPA), when it’s not dealing with exclusions it's facing defense sublimits.

In 2024, employers faced challenges with employee re-engagement. This, combined with social and economic inflation, has added complexity to the risk landscape. Additionally, technological advancements, including the use of AI for candidate screening, have raised concerns about discrimination and liability.

Looking ahead to 2025, retailers should focus on securing comprehensive coverage while remaining vigilant about emerging risks. Ensuring robust policy terms will be crucial for navigating this transitional market.

Insights provided by:

- Kirsty Mitchell, Divisional Director, Amwins Global Risks

The insurance agents’ market is undergoing a period of significant softening, driven largely by increased capacity and a competitive landscape that is suppressing pricing. The influx of new capacity, particularly from managing general agents (MGAs) with experienced underwriters, is reshaping the dynamics of pricing and coverage. While the market is softening with declining rates and increased capacity, agents must remain proactive in addressing emerging risks and securing the best possible terms for their clients.

Capacity and pricing

The market is seeing an influx of new capacity in D&O coverage, primarily through MGAs entering the space. These underwriters are seasoned professionals with strong ties to the market, and their new capacity has created competition that is driving prices down.

The capacity is largely being deployed in excess placements for larger private companies, with some venturing into primary coverage and alternative products. Established market players have adapted to the wholesale distribution strategy by better deploying their capacity, leading to higher limits being offered—often reaching $10M. This heightened competition is also bringing about premium reductions for primary placements, with key carriers aggressively competing to secure business.

The result is a softening market, with 5% to 10% discounts on renewals becoming commonplace. Retentions are decreasing, and underwriters are more willing to offer enhanced coverage to maintain pricing levels. In particular, mid-sized and smaller private companies are benefiting from reduced prices and coverage improvements, especially if they present a favorable risk profile. Even without a compelling risk narrative, many are still seeing lower costs and broader coverage options.

The non-profit segment, however, remains more challenging than the private sector due to historically lower premiums and adverse loss trends. Insurers are finding themselves offering more coverage while accepting less premium in this space, making it a tougher environment for underwriting profit.

Coverage limitations and changes

While coverage limitations have not been widespread, there are notable exceptions. The introduction of biometric information privacy exclusions in states like Illinois and California is one area where coverage is becoming more restrictive.

Additionally, some carriers are tightening exclusions related to insolvency for placements with carriers that have questionable financial health. Concerns are particularly prevalent on the West Coast, where the California FAIR Plan and certain cyber carriers are viewed with skepticism. Insolvency-related exclusions are increasingly being applied to reduce exposure to high-risk accounts, especially in areas like non-standard auto insurance and social services.

A positive trend has been the reemergence of coverage options that were scaled back during the pandemic. More carriers are now offering defense outside the limits, which provides a valuable buffer for policyholders in the event of a claim. Aggregate deductibles are also becoming more common, providing insureds with a more predictable claims experience.

Emerging risks and challenges

The current market stability is being tested by a confluence of risk factors. Volatile pricing in property, casualty, auto and cyber lines is creating uncertainty for agents and brokers. Placing homeowners’ insurance in California remains difficult, especially in high-risk brush zones, while the Florida and Hawaii condo property markets are undergoing significant corrections that could expose E&O policies to new liabilities.

Further complicating the landscape are the risks associated with complex business arrangements, such as third-party administrators (TPAs) and captive insurers. These arrangements have been involved in claims where conflicts of interest arise due to the interconnectedness of the agent, TPA and insurer. The claims severity and regulatory scrutiny in consumer-friendly jurisdictions can present significant exposure for E&O insurers.

Political factors are also adding a layer of complexity. Election cycles have increased scrutiny on placements involving politically sensitive industries. Agents are being pushed to secure coverage for clients in these high-profile sectors, which can be challenging given the already contentious regulatory environment.

Be on the lookout

The market is expected to remain competitive, with pricing continuing to soften due to the abundance of capacity. However, the risk landscape is evolving and insurers are likely to focus on underwriting discipline as volatility persists in certain sectors. Agents should be vigilant about the financial stability of carriers, particularly for placements involving property in high-risk areas or complex multi-party arrangements.

Insights provided by:

- Bill Dixon, EVP, Amwins Brokerage

- Tom Tehan, EVP, Amwins Brokerage

- Steve Vallone, EVP, Amwins Brokerage

Lawyers Professional Liability

The Lawyers Professional Liability (LPL) market continues to navigate a complex landscape characterized by high claim severity, evolving underwriting practices and shifting capacities. Despite these challenges, the market remains competitive, driven by the entrance of new players and underwriters with specialized expertise. These dynamics are forcing legacy carriers to reconsider their pricing strategies and adjust to maintain traction in both primary and excess layers of coverage.

Increased competition

Competition to win both new and renewal business within the LPL market has grown as more experienced underwriters enter the scene. As a result, law firms with strong claims histories and effective risk management practices are often able to negotiate favorable terms.

The push for higher rates and increased retentions is most pronounced among firms with significant claims experience, particularly those operating in high-risk sectors with insufficient risk management controls.

As underwriters seek ways to manage rising claims costs, they are scrutinizing each firm’s risk profile more closely. This includes assessing not only claims history but also risk management practices and the firm’s overall stability.

Capacity and pricing

Capacity remains a critical focus for LPL underwriters as they look to balance growth and profitability. Many law firms have seen significant revenue growth in recent years, and underwriters are using this metric to assess retention adequacy. Although increases in retention are not directly proportional to revenue growth, underwriters are paying close attention to this trend. Retention adequacy has become an essential factor in mitigating the increased claims severity that many LPL markets are experiencing.

In response to the rise in claim severity, particularly claims reaching the excess layers, excess underwriters have begun adjusting their pricing models. To manage long-term profitability, some carriers have reduced capacity, particularly in excess layers. These strategic adjustments are critical in maintaining a healthy portfolio amid rising costs.

Additionally, defense costs for legal malpractice claims have been steadily increasing, with rates rising between 2% and 10%. This presents a challenge for underwriters, as they must find ways to offer competitive terms while managing the escalating costs of defending claims.

Coverage limitations and exclusions

While core coverage in LPL policies remains relatively stable, underwriters are increasingly scrutinizing ancillary coverages and emerging risks. Many policies now include sublimits for trial attendance, disciplinary proceedings and subpoena assistance, often outside the standard liability limits.

Extended reporting periods (ERPs) are increasingly limited to between 36 and 60 months, with true unlimited ERPs becoming rare. These subtle shifts reflect the market’s growing caution amid the environment of rising claim severity.

In addition to traditional risks, LPL underwriters are now focusing on emerging risks associated with new technologies and modern work practices. Law firms’ use of AI, indemnification agreements in outside counsel guidelines and the balance between remote work and office return are under heightened scrutiny.

Further, cyber risks such as ransomware and social engineering have become significant concerns for underwriters. As a result, many are moving toward excluding these exposures from LPL policy forms, opting instead to address them through standalone cyber coverage.

Be on the lookout

As we head into the first quarter of 2025, retailers must be prepared for an evolving underwriting landscape. The influx of new capacity could lead to shifts in underwriting appetites, with some carriers tightening their risk selection processes while others remain open to new business that aligns with their guidelines. The focus on rate increases, particularly for renewals, will continue as underwriters seek to maintain profitability in an environment of rising defense costs and claims severity.

For law firms, it will be essential to maintain open communication with their LPL underwriters, particularly when dealing with succession planning, lateral hires, expanding practice areas or taking on more demanding clients. These changes can significantly impact a firm’s risk profile, and proactive communication is crucial to ensuring adequate coverage is in place.

Insights provided by:

- Bill Schmitt, SVP, Amwins Brokerage

Media

The media insurance market continues to display distinct trends across different regions, with Bermuda remaining a stable choice for coverage and pricing while the domestic landscape presents a more challenging picture.

Companies’ expanding online presence, encompassing websites, blogs and social media, has amplified their exposure to media-related risks, heightening the importance of well-structured insurance coverage.

Understanding the potential gaps that may arise from a change in coverage, and carefully considering policy limits and supplemental coverage needs, will be key factors in managing risk effectively in 2025.

Capacity and pricing

The media insurance market in Bermuda has maintained strong capacity and consistent pricing, with insurers offering reliable options for companies seeking stable coverage in a sector where exposures are becoming increasingly complex.

Domestic carriers have entered the space with attractively low initial pricing, leading some clients to shift coverage for what seems like a better deal. However, such decisions often come with hidden trade-offs, as these providers may not offer comprehensive coverage, and accounts with any claims activity may face non-renewal. This pattern has highlighted the critical need for clients to select insurance partners capable of supporting them over the long term, including during challenging times.

Coverage limitations and exclusions

Coverage terms in the media insurance sector have not seen substantial changes this year, with limitations and exclusions remaining relatively stable across the market. This steadiness can be seen as a positive, allowing brokers to continue offering similar policy structures without having to navigate frequent adjustments. That said, the lack of dramatic shifts should not lead to complacency; insurers may still enforce exclusions or limitations that can materially affect the scope of coverage, particularly in areas such as copyright infringement, defamation and data breaches.

Be on the lookout

Increasing litigation in the space suggests a potential need for higher coverage limits. Given the evolving risk landscape, particularly with companies' growing digital footprints, ensuring that policy limits align with potential exposure levels is crucial. Clients may underestimate the full extent of their media-related risks, including reputational harm and legal expenses, which can have lasting impacts on their business.

Another important consideration is the potential need for complementary coverage, such as cyber insurance. Media exposures often intersect with cybersecurity risks, given the reliance on digital platforms for content distribution and engagement. A media claim could involve a breach of data or a significant cyber event that, if not adequately covered, could lead to serious financial implications. Agents should explore whether bundling media coverage with cyber insurance or other relevant policies could provide a more comprehensive solution to clients. By guiding clients to look beyond initial pricing and focusing on long-term protection, brokers can help ensure that businesses remain resilient in the face of media-related challenges.

The appeal of lower premiums can be strong, but when clients make coverage changes based solely on cost, they risk sacrificing essential protections. Media insurance is a field where unforeseen claims can quickly escalate, affecting a company's financial stability and reputation. Clients should recognize that price alone is not always a true indicator of value, especially in a litigious environment where coverage gaps can lead to significant losses.

Insights provided by:

- Christina Allen, VP Marketing, Amwins Bermuda

The real estate developer market remains active, driven by shifting economic conditions and evolving project demands. The rise in submissions for logistics and distribution projects indicates growth potential in this area and retailers should be prepared for increased demand for coverage.

As development activity steadily continues, the sector faces some ongoing challenges, including fluctuating material costs, regional regulatory pressures and heightened litigation risks. These factors continue to influence coverage options and drive strategic adjustments across the market.

Real estate development continues to expand, particularly in the residential space, driven by housing shortages and expectations of easing monetary policy. Demand for residential projects remains strong; however, commercial development is still under pressure. While there are positive signs as companies encourage employees to return to office settings, the persistence of hybrid work preferences keeps the sector from fully rebounding.

The miscellaneous professional liability (MPL) led insurance approach is favored for developers who contract out design and construction tasks, with coverage largely supported by numerous markets. In contrast, specialized real estate developer forms offer more extensive coverage for firms with in-house design and construction capabilities. These forms address the broader risk profile of integrated firms, positioning them well to manage complex projects and associated liabilities.

Capacity and pricing dynamics

Capacity has grown in recent years, driven by new entrants to the market, and is expected to continue into 2025. This ongoing influx of new capacity has placed downward pressure on pricing, though the extent varies based on the specific coverage approach, and we expect policy terms and language will be altered significantly as a result.

The evolving claims landscape has prompted some carriers to increase rates and retentions, particularly for developers with higher-risk exposures. Florida has emerged as a particularly challenging region due to rapid development and ongoing concerns about construction quality amid frequent storm activity. In addition, New York City’s stringent labor laws continue to complicate coverage placements for construction-related risks.

Limitations and exclusions

Coverage limitations and exclusions have seen minimal changes recently, but ongoing challenges persist. Developers must be vigilant about named insured language due to the complex organizational structures and numerous entities involved in large projects. Many carriers rely on special-purpose vehicle (SPV) wording to streamline named insured lists, but this can inadvertently create coverage gaps if entities are not properly aligned.

Emerging challenges and risks

Economic inflation remains a concern, as high costs for materials affect claims costs and continue to outpace the Federal Reserve's target inflation rate, impacting the affordability of housing and overall project budgets. Additionally, social inflation has intensified litigation risks in the residential sector, particularly for class-action lawsuits against developers.

The commercial office sector faces distress due to changing work habits, which has complicated the placement of general liability policies for projects in this space. Conversely, developers focusing on rental properties may find opportunities as housing affordability remains challenging, pushing more people towards renting rather than buying.

Be on the lookout

A standard D&O policy is often limited in coverage compared to a well-structured Real Estate Fund E&O/D&O form, creating an opportunity for brokers to provide enhanced value in this space.

As the market matures, it will be essential for retailers to stay informed about emerging trends, new capacities and coverage intricacies to effectively support their clients. Working closely with expert partners will be key to navigating this specialized segment in the coming year.

Insights provided by:

- Craig Dunn, EVP, Amwins Brokerage

- John Grise, EVP, Amwins Brokerage

- Trey Waldrep, VP, Amwins Brokerage

- Augie Yost, VP, Amwins Brokerage

Reinsurance

Property

As we look to the January reinsurance renewal season, rates are expected to remain stable overall, with the potential for lower premiums on accounts without losses. This is in large part due to market corrections following an intense period of hardening throughout 2023.

The restructuring of reinsurance programs to raise attachment points while tightening event definitions and hours clauses has shifted reinsurance protection away from frequency protection and towards severity coverage. While repricing has been a significant part of that, reinsurers are still telegraphing a refusal to negotiate on retention levels as they assume less exposure for more premium and primary insurers shoulder the bulk of catastrophe losses.

We also don’t expect Hurricanes Helene and Milton to have a material impact on the market.

Facultative property reinsurance

Treaty renewals in 2024 were more organized than in 2023, bolstering most markets’ confidence and ability to quote capacity – even in high hazard CAT zones. At the same time, there continues to be limited appetite for attritional business and a focus on secondary perils.

The market has begun to soften with supply starting to outweigh demand on direct placements. Renewals in Q2 saw double digit reductions as a result and there has been less flexibility in terms and conditions. For example, the average/margins clauses that were added in 2023 have been removed from a large proportion of 2024 renewals.

London

At the peak of last year’s hard market, London made it clear that the 2024 business plan would include a renewed focus on providing capacity to the property market. As a result, the facultative market has seen increased competition and a new downward pressure on rates as Lloyd’s looks for new and creative ways to book premium.

The facultative reinsurance market is typically slower to react to these shifts in pricing and we saw a disconnect between direct and reinsurance pricing. This resulted in relatively expensive reinsurance capacity being more difficult to sell, as direct rates fell at a faster rate than reinsurance rates.

Casualty

In general, research suggests social inflation could be causing losses to increase faster than general inflation by 2% to 3% per year. And, as a result, reinsurers are either holding the line on rate or implementing slight increases just to keep up.

Facultative casualty reinsurance

The facultative reinsurance casualty market is in a state of transition. E&S capacity is more readily available to casualty risks as new carriers and MGAs have entered the space, and carrier treaty renewals at 1/1, 4/1 and 5/1 were more organized than in 2023, bolstering the direct markets’ confidence and ability to quote capacity.

As a result, competition for large facultative placements is significant in less distressed areas of the casualty marketplace. However, for some of the more difficult to place accounts, facultative reinsurance is in demand, with reinsurers eager to retain renewals as well as write new, profitable business.

Treaty reinsurance

Increased retentions and the rise of losses due to secondary perils has seen many insureds bear the brunt of 2024 property losses. Reinsurers, however, have benefited from reductions in coverage and increased deductibles. Conversely, this redistribution of loss in 2024 has had a negative impact on insurer balance sheets and therefore some recalibration for 2025 is expected (provided projections of loss from Hurricanes Helene and Milton remain minimal).

Casualty rates are set to increase in 2025 and concerns from global reinsurers about adequate reserves juxtaposed against the rise of nuclear verdicts paint a concerning picture. We expect there will likely be a reduction in available capacity as some reinsurers exit the segment.

Be on the lookout

Most industry experts agree that Hurricanes Helene and Milton will have a muted impact on the reinsurance market. While not expected to raise rates, any potential market reductions are expected to slow. The storm’s likely low impact on reinsurers will likely strengthen their resolve around retention levels.

Reinsurance markets appear to be more attentive to SCS losses than wholesale or retail markets. However, with unparalleled access to modeling and data, they can pivot quickly and find new fronting capacity when carriers may not be able to.

The rise of economic inflation has slowed; however, operational costs and claims have been affected, complicating accurate risk assessment. Similarly, advancements in AI and data analytics are reshaping the marketplace and directly impacting how risks are priced.

On a global scale, one of the biggest concerns for 2025 is socioeconomic systemic loss arising from increased political violence and civil unrest. As new risks and exposures emerge, both financial and societal, insurers will need to consider the level of protection they are willing to offer.

Insight provided by:

- Jennifer Del Re, President of Amwins Re

- Lee Jon El lis – Head of Portfolio Reinsurance Solutions, Amwins Global Risks

- Tom Jakob – Director, Worldwide Property, Amwins Global Risks

Construction

Builders’ risk

While the number of new entrants into the market has slowed from last year, most regions are still enjoying surplus capacity fueled by both carriers and London Syndicates. The exceptions to this are Florida, Coastal Louisiana and Coastal South Carolina, where capacity had already been more difficult to come by before the effects of Hurricane Helene are fully realized. The New York market has improved from last year, with relative stability and renewals seeing mostly flat pricing to 10% increases. Wildfire business continues to see limited market capacity as well as higher rates and deductibles.

Overall, there is ample capacity producing downward trends on pricing. We are also seeing the beginning of softening deductibles and relaxed project-lifecycle conditions, including guaranteed extensions, occupancy and escalation. There are some moves from markets to protect their capacity; for instance, in London, many markets are cutting back limits on layered deals, such as from $10M to $7.5M or $5M. However, this has not had a significant impact on the market.

Casualty

Strong capacity exists in primary GL markets for straightforward placements and lower hazard classes with good loss history should look for flat to low single digit renewal rates this year – except in New York where markets are still looking for 5% to 10% renewal increases. Tougher classes (demolition, curtain wall, foundation and scaffolding, as well as excess capacity on frame for-sale residential construction in construction defect states) do have fewer options, but coverage can still be readily found.

In excess, there is increased competition for layers between $5M and $10M, and towers of $50M or more should at worst see flat premiums. As in primary layers, flat to low single digit renewal pricing is common, compared to double-digit increases a year prior.

Auto liability is a challenging line, as it is in other segments. Both economic and social inflation continue to drive up auto claims costs, especially in litigious venues such as Texas, Florida, California, New York and Washington. Heavy auto fleet contractors in particular are looking for higher auto attachments.

The professional liability market in the construction space is stable and competitive. Historical classes such as condos, unique energy risks (solar facilities, battery plants, geothermal sites, etc.) and integrated project delivery (IPD) continue to be challenging, especially in Florida and New York, which are loss leaders for the markets. Capacity remains available for Architects & Engineers as well as Contractor’ coverage. And despite a few new entrants to the market over the past few years, pricing is relatively unchanged. Social inflation continues to play a role in underwriting costs; however, most agree that those increases have already been baked into renewal pricing.

Be on the lookout

Falling interest rates should drive even stronger interest in home sales, and developers and builders are already responding with more new construction starts. Be aware that some of the larger general contractors are starting to require subcontractors to carry TRIA (Terrorism Risk Insurance Act) coverage.

Get ahead of carriers making wholesale changes to their book, especially carriers who play in a lead capacity space.

Insight provided by:

- Jett Abramson, EVP and Casualty National Construction Practice Leader, Amwins

- Brett Fowler, VP, Architects and Engineers Program, Amwins Program Underwriters

- Scott Jensen, EVP and National Construction Practice Leader – Casualty, Amwins

- Gary Keenan, Managing Director, Construction Division, Amwins Global Risks

- Gary Dennis Ricker Jr., EVP and Casualty Construction Practice Leader, Amwins

Energy

Since 2023 the energy market has begun to see signs of recovery. However, catastrophic events and ongoing technological advancements that complicate coverage, particularly in the power and solar markets, have slowed progress. Conversely, the professional and property lines have begun to experience some relief.

Downstream energy

Following historic highs in 2023, premiums within the downstream energy property sector have stabilized. With fewer significant losses and limited natural disasters, insurers have become more profitable and, when combined with ample supply, this has created a more favorable environment for insureds.

The financial burden of rising insurance costs is still a concern, especially as the frequency and severity of SCS increase. The 2024 windstorm season was particularly active, and wildfires have already burned

significantly more acreage than in 2023. The market's response to these conditions remains uncertain, especially in the wake of hurricanes Helene and Milton.

The downstream energy property market is showing signs of softening, with projected rate decreases between 2.5% and 7.5%, a welcome change after last year’s increases of up to 30% for insureds with substantial losses. Meanwhile, the downstream casualty market has experienced a significant number of claims over the past 12 months, leading to continued pricing increases amid limited market capacity.

While the rates in the downstream property sector have begun to decrease from their highs, the rates in casualty have turned the other direction. Markets have continued to decrease capacity and that, combined with new losses, has accelerated the pace at which rates have grown over the past six months. We expect this trend will continue into 2025.

Power dynamics

The casualty market within the power sector is experiencing shifts as major players exit, leaving gaps for new entrants to fill. While some stabilization has occurred, the sector hasn't softened as quickly as other areas. The demand for power is escalating due to factors like population growth, climate change and cryptocurrency mining, as well as the rise of electric vehicles and AI. This surge in demand is outpacing the existing supply infrastructure, emphasizing the need for robust partnerships.

Battery storage installations are also increasing and insurers are becoming more accommodating for proven technologies with strong loss controls. However, new technologies lacking established loss mitigation strategies face a challenging insurance landscape.

Solar power growth

The boom in solar energy installations has been fueled by technological advancements and further investments in clean energy. However, increasing hailstorm severity poses a growing risk to solar farms, which are often located in exposed areas. The potential for significant hail-related losses is a major concern as more high-value assets come under threat.

Midstream sector challenges

While downstream energy property is stabilizing, the midstream sector faces increased competition from new facilities and ongoing M&A activity. Regulatory constraints have slowed large M&A transactions – smaller transactions are now the norm.

The casualty market remains challenging due to rising claims and nuclear verdicts, which drive up premiums while reducing available capacity. The excess energy market is continuing to harden, with rates pushing 10% to 15% across the board on loss free accounts.

Capacity appears to be tightening, often reducing lead capacity to $5M or less, with instances where a lead $10M or $15M policy is reduced to $5M for a similar premium. For auto-heavy accounts, there is a growing necessity for buffers or lower limits, typically in the range of $2M to $3M. These changes stem from the rise in adverse claims, leaving the potential for opportunity as terms and limits tighten.

Upstream capacity constraints

The upstream energy market is grappling with demand and supply challenges, particularly for traditional energy sources like coal and gas. Texas and Louisiana remain critical jurisdictions for energy accounts, but overall market conditions are tightening, complicating coverage availability.

Environmental, social and governance (ESG) pressures are constraining supply, leading to rising material costs. Furthermore, two major insurers have significantly reduced their presence, exacerbating capacity issues and driving up pricing.

Professional lines and cyber market trends

In professional lines, D&O insurance rates are favorable, with solid capacity available. Companies with strong financials may even see aggressive pricing and double-digit rate decreases. Conversely, debt-leveraged insureds could face challenges as underwriters focus on financial stability.

Premiums continue to decrease significantly in the cyber insurance market despite rising claims activity. Underwriters are optimistic about renewals, although challenges persist with ransomware and an uptick in class action lawsuits related to data privacy.

London

While the London market is beginning to show signs of a slight softening, the overall landscape remains challenging due to rising claims and costs. Social inflation remains a growing issue, as court-awarded payouts have risen significantly. Insurance policies that once required $5M in coverage may now need up to $15M.

Insights provided by:

- Ben Abernathy, VP, Amwins Brokerage

- Rob Battenfield, EVP, Amwins Brokerage

- Tim Collado, VP, Amwins Brokerage

- Craig Dunn, EVP, Amwins Brokerage

- Johnny Hilliard, Divisional Director, Amwins Global Risks

- Samuel Outram, Divisional Director, Amwins Global Risks

Environmental

The environmental market continues to be stable on balance. Although some carriers have exited the space, new entrants have offset their departure, helping to limit drastic rate swings or notable new exclusionary language and keep conditions competitive overall.

Specific classes or regions

Environmental clients are generally enjoying soft market conditions, but there are exceptions. In the nonhazardous solid waste market, policy terms, conditions and pricing have tightened, with some markets no longer writing business due to adverse experience. In Texas and Louisiana, several carriers have restricted their appetite to limit exposure to contractors operating in industrial facilities as well as the oil/gas sector. Some carriers have also pulled back on downstream energy risks.

Auto is problematic across this segment. Accounts with heavy fleets, such as recycling, hydrovac or soil remediation, are facing very limited options, particularly in excess coverage. The cause is the same as in commercial auto in general: social inflation, litigation funding and other factors behind nuclear verdicts driving up loss costs.

Capacity and pricing

For monoline pollution products (CPL, Site Pollution and Contractors E&O/Pollution), the market is robust with flat pricing. Contractors’ pollution liability is competitive, with more than 50 markets willing to write the coverage, including annual practice policies or OCIP/CCIP pollution wraps and project policies. Several carriers are offering up to five-year policy terms on site pollution.

In combined form GL/Pollution/Professional/Products, several markets have cut capacity and raised rates, depending on the location and services of the risk being insured. In excess, while numerous markets will offer unsupported coverage, several have pulled back on limits offered, requiring more carriers to build the same tower. Typically, 5x primary are the highest limits available, and sometimes less if the carrier offers companion auto to go with the program. In supported excess, several markets have pulled back limits offered, with some now only offering short leads or no excess at all when they write GL/Pollution and auto.

Limitations and exclusions

Like the emerging trend last year, PFAS (perfluoroalkyl or polyfluoroalkyl substances) exclusions are increasingly mandated by carriers; however, there are markets willing to modify or remove the exclusion for contractors and consultants who are working on cleanups. Additionally, a few markets are willing to provide coverage for an insured’s site if they can demonstrate that they have little to no exposure to PFAS chemicals. Wildfire coverage is also becoming more difficult to obtain dependent on the insured’s location and operations.

Additional impacts affecting clients

The EPA finalized its designation of perfluorooctanoic acid (PFOA) and perfluorooctane sulfonate (PFOS) as hazardous substances under section 102(a) of the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA). This gives the EPA enforcement power against responsible parties that manufactured these chemicals as well as certain federal facilities and other industrial parties. Ethylene oxide (EtO) continues to remain as a potential issue to monitor as well.

The EPA’s environmental justice initiative, which focuses on cleanup efforts in low-income and disadvantaged communities, is leading to increased fines and scrutiny for accounts operating in these areas. Additionally, non-governmental organizations, often backed by third party litigation funding, are increasingly filing lawsuits against alleged polluters.

Be on the lookout

There are several new entrants to the market that will offer combined form GL/Pollution/Excess, while others are focused on Site Pollution/Contractors Pollution/Contractors Professional/Pollution. Given the wide variations in coverage forms, careful analysis is needed to assess the quality of these products and any lurking limitations or exclusions.

Insight provided by:

- Susan Diecidue, AVP and Underwriting Manager, Amwins

- Daniel Drennan, VP, Amwins Brokerage

- Tom Graham, Director-Casualty, Amwins Global Risks

- Forrest Leary, SVP, Amwins Brokerage

- Bryan Mierzwinski, Associate Director, Amwins Program Underwriters

- Brett Pollard, VP, Underwriting, ALTA Risk

Healthcare

Hospital margins have improved over the past year: the median YTD operating margin reached 5% in May 2024, a substantial increase compared to just 0.7% in May 2023. However, long-term financial challenges persist. Greater labor and supply expenses, as well as rising patient acuity requiring longer hospital stays, continue to challenge facilities. Private equity's growing role in healthcare also adds to regulatory scrutiny of pricing and care quality.

Despite current buyer-friendly market conditions overall, care facilities should focus on operational efficiency and partnering with well-capitalized entities to mitigate risks. Attention to revenue diversification and reducing reliance on government funding will also be important.

Specific classes and regions

Urban hospitals have seen financial improvement recently, but rural hospitals remain in distress due to severe financial issues, with many at risk of closure. Higher labor and supply costs, along with structural workforce shortages, are key drivers.

Physician groups, nursing homes and allied health facilities also face ongoing financial pressures. Physician groups in particular are grappling with the administrative burden of the prior authorization process, which impacts physician burnout and patient outcomes.

Nursing homes are struggling with labor shortages and operational pressures; however, insurance pricing for skilled nursing accounts in friendly legal venues is starting to decline. In long-term and senior care, better risks should be able to find stable or slightly favorable pricing where competition is increasing. However, others will find it difficult to obtain attractive terms, particularly for risks with an adverse loss history or those in litigation-prone venues.

Capacity and pricing

As losses continue to outpace premiums, underwriters would like to obtain renewal increases. However, market competition overall is instead producing flat premiums to single digit decreases and this trend is expected to continue into 2025. Premium pressure is not being driven by new capacity but, rather, increased competition (particularly on larger accounts) as established markets try to increase market share. The exception is excess liability, where capacity continues to be limited and care facilities can expect to see umbrella increases of 30% or more.

Limitations and exclusions

Reinsurers continue to push for SAM limitations or exclusions. As a result, primary markets are pulling back on limits and/or offering coverage only via a limited supplemental abuse endorsement. Obtaining affirmative coverage for SAM in excess layers is difficult. Underwriters also maintain their push for hired and non-owned auto exclusions.

As more carriers without tailored healthcare forms enter the market, buyers and retailers should be cautious about lower premiums that may signal limited coverage or financial risk from newer, less established carriers. They must also evaluate whether a carrier is financially stable and has a strong track record for paying claims.

Additional impacts affecting clients

As in other sectors, social inflation is leading to increased severity of claims and higher losses, driving costs up significantly and keeping pricing and terms from improving even more than they already have. The list of litigation hotbeds for healthcare providers continues to grow as states that used to be less litigious are now becoming more active.

In this environment, the concern is that carriers chasing market share will not be able to sustain pricing, and insureds will be faced with steep increases in the near future, which can be harder on a care facility’s business than long-term stable pricing.

Be on the lookout

While larger healthcare organizations, such as hospitals and health systems, typically work with reputable healthcare carriers and are willing to potentially pay a higher premium to ensure they get the most comprehensive coverage, the number of competitors in this space has grown, continuing to drive premiums down. It’s important to recognize that not all carriers offer specialized healthcare forms, and cheaper prices may come with reduced coverage or exclusions.

Healthcare organizations' financials have improved significantly; however, they are not yet out of the woods and financial solvency needs to be sustained. Increased scrutiny regarding private equity ownership in healthcare facilities is likely to continue, and labor shortages and rising supply costs remain ongoing concerns.

Insight provided by:

- Jordon Connelly, EVP, Amwins Brokerage

- Don Tejeski, EVP, Amwins Brokerage

- Yajaira Villegas, SVP, Amwins Program Underwriters

- Matthew Wasta, FCAS, VP, Amwins Program Underwriters

Public Entity

Legal, technological and actuarial factors are playing a key role in the growth of the public entity landscape. Understanding these shifts is crucial for public entities and insurers to effectively manage risk and adapt to changing conditions. Key trends and dynamics are emerging across areas such as casualty, property, crime and cyber insurance, with important considerations for the coming year.

Property

The public entity property insurance market experienced some relief in 2024, with increased competition driving rate decreases for well-managed, loss-free accounts. This trend was most evident in primary and lower excess layers, while high excess layers remain constrained. Catastrophic events, however, continue to pose significant challenges, underscoring the importance of data collection and modeling advancements.

Hurricane Milton brought significant damage across the Gulf Coast, particularly in coastal areas while Helene was more impactful in non-coastal regions of the Southeast. While claims are still coming in and the full impact remains uncertain, early indications suggest that the extent of losses will be lower than those from Hurricane Ian in 2022. High winds, heavy rainfall and storm surge caused widespread destruction, with some areas still recovering from previous storms. Although Milton will likely be among Florida's costlier hurricanes, the market is not expected to face the same level of disruption experienced after Ian.

Overall trends continue

Requests for higher limits, enhanced coverage and lower deductibles have increased as entities look to bolster financial protection. Enhancements to a program's terms and conditions are another way to improve a program in the current market. Focusing on changes other than pricing will help incumbent markets navigate the renewal versus being solely a price-driven transaction. There is potential to remove/adjust vacancy endorsements, roof valuation endorsements and margin clauses to ensure more consistent coverage across the panel of markets.

The integration of RMS 23 alongside RMS 21 modeling is providing insurers and public entities with a better understanding of potential impacts, which is crucial given increased storm activity. Understanding the impacts of RMS 23 versus RMS 21 is vital as you look to build a successful renewal strategy.

Strategic renewal approaches

Successful renewals hinge on employing specialized strategies, such as reconfiguring insurance programs, engaging with new markets and fostering strong underwriter relationships. This approach is particularly important in navigating the complexities of high excess layers, where capacity remains limited.

We expect the January 1 reinsurance market will also reflect the impacts of Hurricanes Helene and Milton. At what level, remains to be seen.

Casualty

The casualty sector continues to contend with an increasingly challenged legal environment, limited lead layer market alternatives and constantly evolving liability exposures. Factors such as ongoing policing reforms, tort protection and immunity erosions, reviver statutes for abuse claims and overall staffing shortages have adversely impacted liability loss severity trends and ultimate claim values, particularly for law enforcement, street and road design, as well as auto risks.

Trends and dynamics

While there are signs of stabilization in premiums, retentions and limits for best-in-class risks, the market still faces challenges with excess layers. Social inflation and nuclear verdicts continue to drive up costs and historical payback considerations are being re-evaluated, while pressure for increased intervening layer premium relativities increase total costs of risk transfer.

Geographic diversification efforts have led to varied rate changes across regions, making it essential for insureds to present complete and detailed submissions to secure favorable terms.

Litigation funding and risk management

Third-party litigation funding is increasingly influencing claim values and litigation patterns. As a result, underwriters are scrutinizing submissions more closely, and actuarial involvement in pricing determination has become more significant. Risk management innovations, such as predictive analytics and incident reporting technologies, are becoming critical tools for mitigating exposures and controlling loss costs.

Cyber

The cyber insurance market for public entities remains cautiously optimistic despite increased claims activity, particularly from ransomware and e-crime incidents. While rates have mostly remained stable, carriers are concerned about aggregation issues, as highlighted by incidents involving major firms like CrowdStrike. Public entities with robust cybersecurity practices can still secure competitive terms, but those lacking controls like Multi-Factor Authentication (MFA) may face limited options and sub-limits.

Claims trends

The frequency of ransomware demands and e-crime claims continues to rise, with hacker groups becoming more aggressive. To counteract these risks, carriers are emphasizing cybersecurity services for policyholders, including training and risk assessments. Pools remain a popular option for public entities due to lower premiums and retentions compared to standalone policies.

Future projections

Looking ahead, the market may see changes following reinsurance renewals, which could lead to rate adjustments. Continued threats, including large-scale cyberattacks and email compromise incidents, are anticipated in 2025. As markets narrow their distribution to specialists with niche expertise, new entrants will likely focus on smaller public entities or limited distribution channels.

Crime

The crime insurance market for public entities remains a niche sector with a limited number of carriers specializing in areas such as faithful performance of duty coverage. The coordination between cyber and crime coverage for e-crime claims remains challenging, as overlapping policy provisions can create gray areas in coverage.

Underwriting considerations for 2025

Expect more underwriting questions related to e-crime exposures and employee training practices. Carriers may introduce exclusions to address these risks, making it critical for insureds to maintain both crime and cyber e-crime coverage to avoid coverage gaps.

Bermuda

The Bermuda market continues to be an important source of property and casualty capacity for public entity clients, particularly where capacity is needed to fill gaps in a tower.

The property space has become softer with clients seeing flat renewals or in some cases, rate decreases in the 5% to 10% range. The impact of Hurricanes Helene and Milton are yet to seen, but this will become clearer through the January 1 reinsurance renewal season.

Casualty rate increases are still the norm but are now more likely to be single digit, except for accounts with adverse loss history. Markets in Bermuda have had the most success filling gaps in towers with small amounts of capacity deployed.

Be on the Lookout

- Property: High excess layers will remain a challenge as market capacity struggles to keep up with demand. Keep an eye on new entrants and advances in catastrophe modeling, as these can provide better pricing opportunities and improved coverage terms. The impact of Hurricanes Helene and Milton remains to be seen.

- Casualty: Watch for continued shifts in the legal landscape, particularly in states undergoing policing reforms or enacting new legislation. Expect more scrutiny from underwriters, especially regarding third-party litigation funding's impact on claim values.

- Cyber: We anticipate potential rate increases and stricter underwriting guidelines following January’s reinsurance renewals. Stay vigilant about ransomware trends and reinforce cybersecurity measures, including employee training and endpoint protection.

- Crime:Look for more detailed underwriting requirements around e-crime exposures and anticipate potential exclusions as carriers refine coverage terms. Maintaining comprehensive crime and cyber policies will be essential to mitigating risk.

Insights provided by

- Brian Frost, EVP, Amwins Brokerage

- Ali Hoefle, VP, Amwins Brokerage

- Darron Johnston, EVP, Amwins Brokerage

- Alan Mooney, CEO, Amwins Bermuda

- Dave Weller, EVP, Amwins Brokerage

Real Estate

Property Segment Trends and Pricing

What a difference a year makes